We love shortcuts. Whether using CTRL+C/CTRL+V for copy and paste or finding the shortcuts, we are always looking to optimise how we spend our time and energy. Our brain does this too; without using any mental capacity, we know to buy low and sell high, and we make thousands of other decisions based on heuristics, or shortcuts, where the answer just feels right.

But these shortcuts can also lead us astray – and that is when they become biases. A Morningstar study looking at the importance of behavioural biases when making investment decisions found that relying on intuition often leads to investment errors. What’s more, “The Financial Impact of Behavioral Biases” study found that 98% of people in the U.S. exhibit at least one bias.

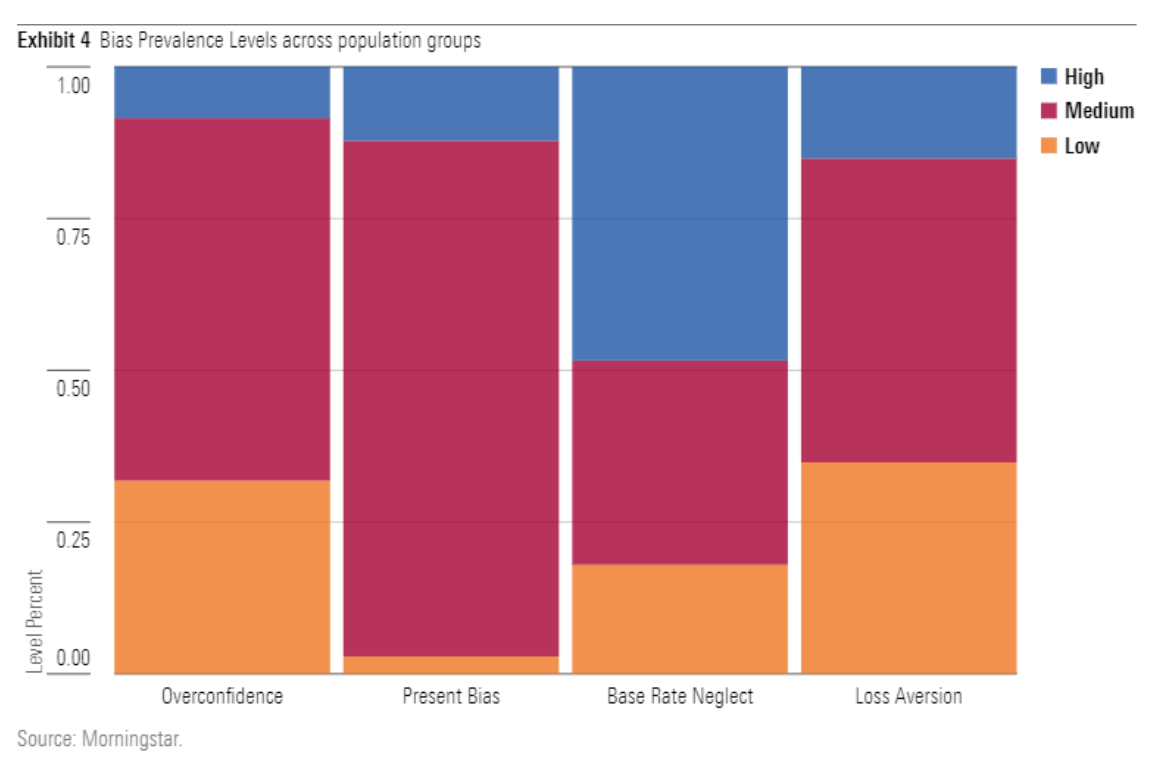

The research found that the majority of Americans show biases across four categories:

- Present bias: The tendency to overvalue smaller rewards in the present at the expense of long-term goals (think Marshmallow Test).

- Base rate neglect: The tendency to judge the likelihood of a situation by considering new, readily available information about an event while ignoring the underlying probability of that event actually happening.

- Overconfidence: The tendency to overweigh one’s own abilities or information when making an investment decision.

- Loss aversion: The tendency to be excessively fearful of experiencing losses relative to gains and relative to a reference point.

More Bias = Worse Outcomes

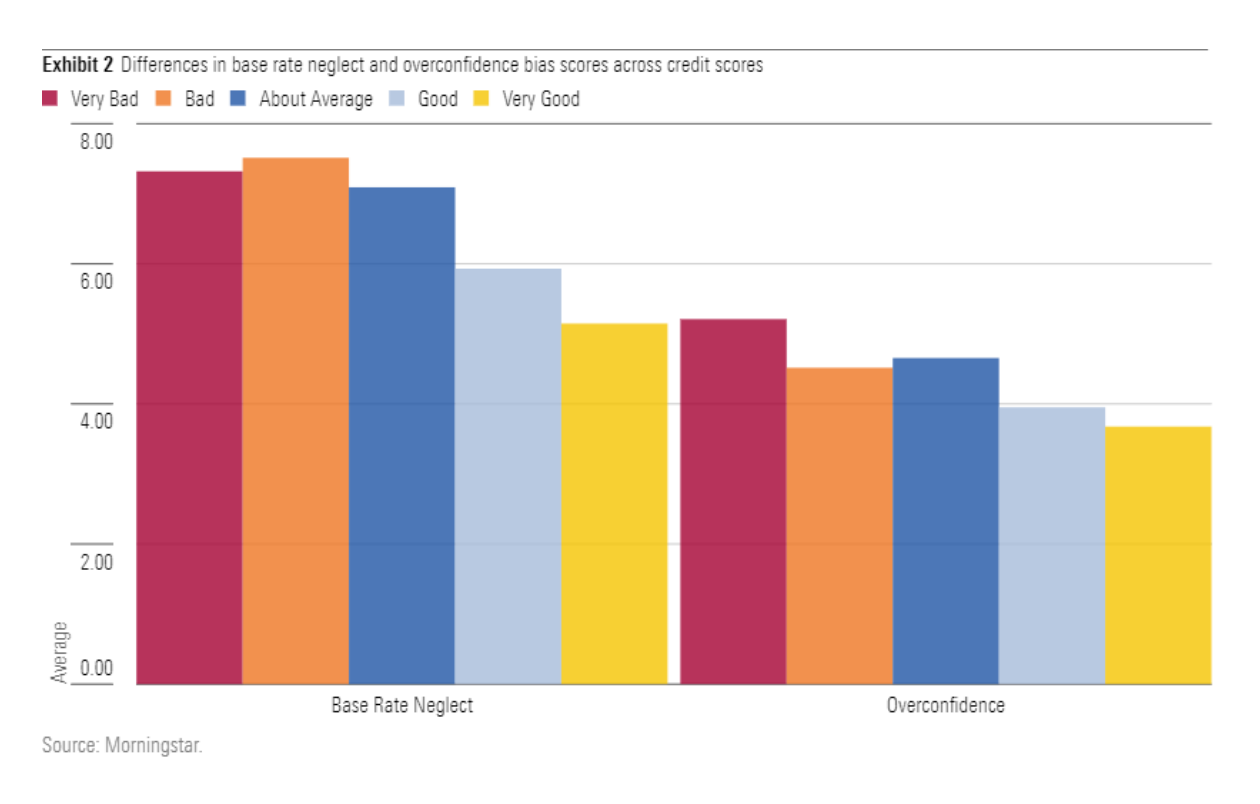

The higher our bias score, the worse our financial outcomes. There is a direct correlation between higher bias scores and worse financial health scores, bad credit scores, lower account balances and higher debt.

But Morningstar analysts found that bias does not seem to be explained by demographics, or characteristics like financial health or numeracy. Rather, it is linked to certain behaviours like failing to plan ahead or to save and invest, which then manifest lead to sub-optimal financial choices.

For example, people with high base rate neglect bias were 11 times more likely to have a bad or very bad credit score. Meanwhile, people with high overconfidence — particularly Gen Z and millennial investors — were eight times more likely to have a bad credit score.

With 98% of investors holding at least one biased opinion, it is clear that bias is more than an abnormality; it is a universal tendency. But by identifying biases and connecting them to real-world outcomes in a financial context, investors can understand the importance of mitigating these shortcuts.

Luckily there are ways to change our thought processes in order to hinder our biases in making snap decisions for us, and researchers have spent decades on figuring out ways to outsmart them. Three habits in particular can help protect us from ourselves:

3 Ways to Ban Your Biases

Setting up decision-making speed bumps

Slow down the decision-making process by setting up decision-making “speed bumps". These help us avoid impulsive decisions and let us take a step back from our emotions. For example, work to create a three-day wait rule before you buy or sell a stock (where you can’t act on a decision for three days) or perhaps ask a loved one or spouse to sign off on any major decision before you act.

Objective trading rules

Set objective trading rules that never change. For example, if the stock rises above a certain level, set a trailing stop that will lock in the gains. Consider working with a financial adviser to formulate a written investment policy statement. This can prevent you from making irrational decisions during times of economic stress or euphoria.

Ignore the news

Try to ignore the daily news when it comes to investing. Make the effort to ignore irrelevant information, particularly short-term price movements, and instead keep your eye on the bigger picture — and seek out information that lends itself to making that bigger picture clearer, don't end up in an echo chamber of views that tell you what you want to hear.

Biases are a natural part of how our minds are wired, and from the research, it is clear how prevalent it is in the American population, across different socioeconomic backgrounds. And, these biases can do real harm, so by making an active choice to recognise our mental shortcuts we can take steps to not just improve our investment returns, but better our credit scores, net worth, saving and spending habits.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/5FNGF7SFGFDQVFDUMZJPITL2LM.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EOGIPTUNFNBS3HYL7IIABFUB5Q.png)