In part 1 of this article looked at how the low-volatility ETFs have performed in the market downdraft. In this part, we will examine the differences among them.

Results May Vary

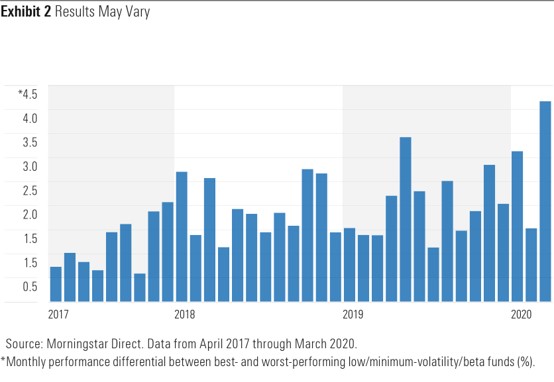

There are important, albeit nuanced, differences in the way low-volatility strategies are constructed. The disparity in USMV and SPLV's recent performances is a testament to that. Exhibit 2 provides further evidence. It shows the absolute value of the spread in the monthly performance of the best- and worst-performing funds among the eight U.S. large-cap low-volatility ETFs over the three years through March.

The Case of USMV Versus SPLV

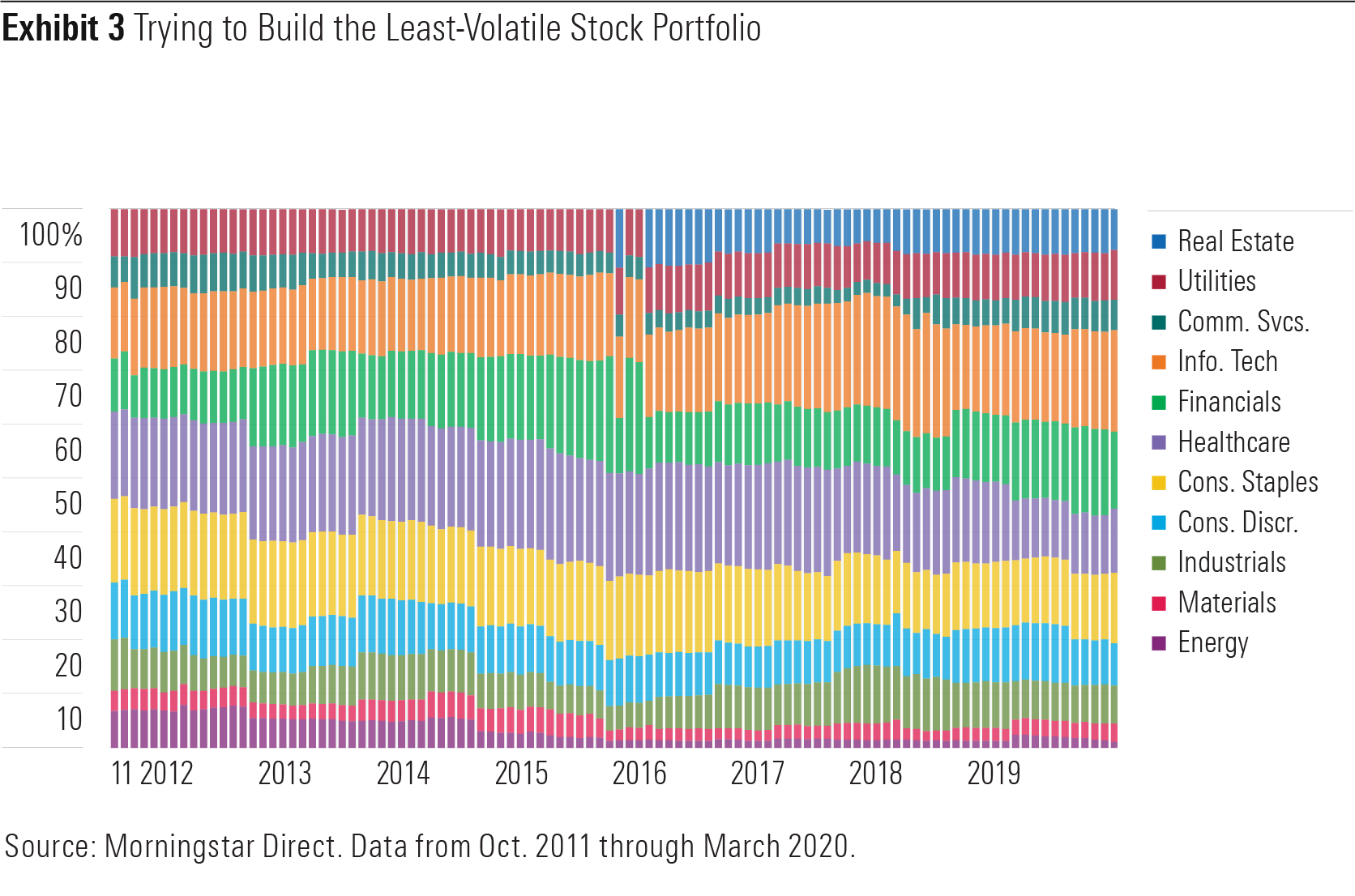

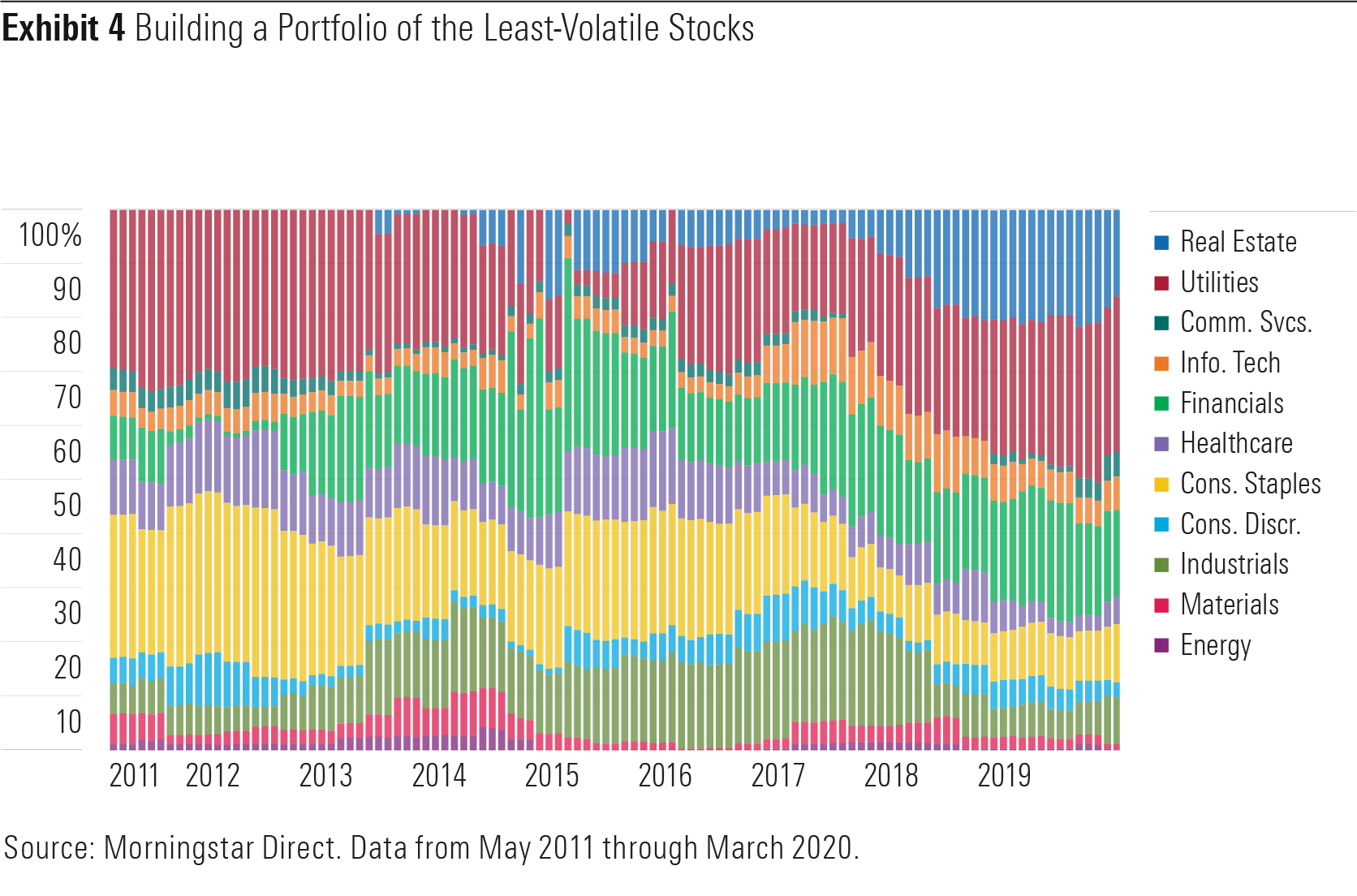

In the case of USMV and SPLV, these differences point back to the funds' overarching approach to portfolio construction. USMV attempts to build the least-volatile portfolio of stocks it can, choosing from the MSCI USA Index. SPLV's portfolio is made up of the 100 least-volatile stocks from the S&P 500. There's a distinction between combining stocks to form the least-volatile portfolio versus building a portfolio of the least-volatile stocks. At first blush, it may seem trite, but the complexion of these funds' portfolios is markedly different.

Exhibits 3 and 4 show the evolution of the funds' GICS sector exposures. The comparison illustrates the differences in their approaches. USMV's sector exposures are relatively stable. This is because its index tethers its sector weightings to those of its parent index. They can't stray more than 5% in either direction from this reference point. SPLV has no such restrictions in place, which can lead to large and persistent sector bets.

At the height of the market in mid-February, utilities and real estate stocks made up nearly 47% of SPLV's portfolio. At that time, stocks from those same two sectors represented just 17% of USMV's portfolio. SPLV's exposures in these sectors explained just over half of its relative underperformance versus USMV from the mid-February peak to the late-March trough.

Methodological differences between these seemingly similar funds are important to understand, as they can lead to material differences in their long-term risk and return profiles.

Less Volatility

Low volatility does not mean no volatility, just less. Low-volatility stock funds are still stock funds. They are designed to be less volatile than their selection universes, and there's no question that they have delivered based on that criterion. But it can be dangerous to equate "less" volatility with "low" volatility. The former is a more apt description, and one that would better calibrate investors' expectations. The latter better describes assets that would better diversify equity risk, like high-quality bonds.

The most promising feature of these funds is that they could--in theory--help investors stay in the market during trying times, dulling the pain they experience each time they check the value of their portfolio. But I'm deeply skeptical that they can serve that function. I don't think most investors take comfort in losing relatively less when the market hits an air pocket.

Investors need to understand that while these funds may have a place in their risk-management tool kit, they are specialized implements. Less-volatile equity portfolios may have a place, but they rank well below setting aside a rainy-day fund, having an appropriate asset allocation, and going for a walk outside the next time you're tempted to tinker with your portfolio.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/5FNGF7SFGFDQVFDUMZJPITL2LM.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EOGIPTUNFNBS3HYL7IIABFUB5Q.png)